Why USDat Yield is Stable

A deeper look at where USDat’s yield comes from - and why its design makes it scalable and durable across market cycles.

USDat Yield: Built for Scale and Safety

The Shift: From DeFi Borrowers to Institutional Bitcoin Credit

Bitcoin Credit is not a new concept. For years, users have been able to borrow against their Bitcoin and pay interest over time through DeFi protocols. However, that landscape of Bitcoin-based credit in DeFi faces three major limitations:

Collateral instability: No existing protocol/borrower has effectively managed Bitcoin’s volatility in a scalable and suastainable way.

Limited demand: DeFi users alone has not generated sufficient demand for Bitcoin credit.

The emergence of Bitcoin Treasury companies (BTC DATs) marks a turning point in Bitcoin credit as crypto and TradFi converge.

Companies like MicroStrategy have become major institutional borrowers using Bitcoin as collateral.

As public companies with access to deep capital markets, they can withstand Bitcoin’s volatility, making institutional-scale Bitcoin collateralization viable for the first time.

Why the Yield Is Scalable

At its core, USDat generates yield by lending capital to MicroStrategy, and over time, to other Digital Asset Treasuries (DATs), at a floating annual interest rate of 10.25%. MicroStrategy uses this borrowed capital to iteratively purchase Bitcoin.

When Bitcoin appreciates, MicroStrategy repays its loans using capital gains from its holdings. This structure creates a natural spread between Bitcoin’s long-term compound annual growth rate and its cost of capital (the interest paid to USDat), forming what we call the Bitcoin Carry Trade.

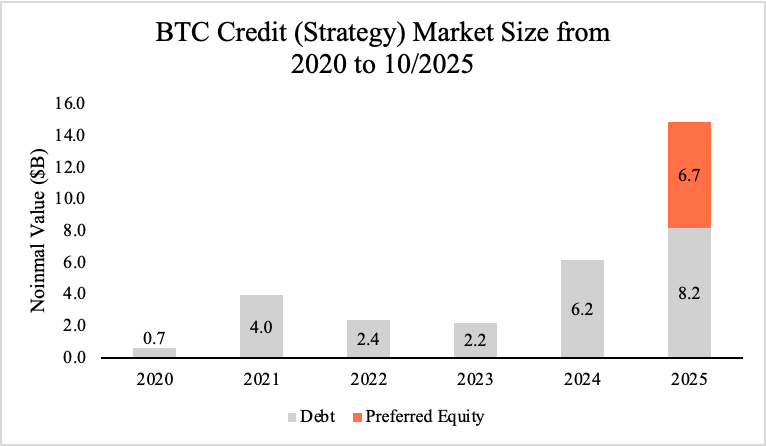

To put the credit opportunity from this Bitcoin carry trade in perspective, the total market centered around Strategy is exploded from approximately $700M in 2020 to $14.9 billion in 2025, growing at a compound annual growth rate of 85% since 2020.

Source: Strategy’s 2020-2025 Quarterly Reports

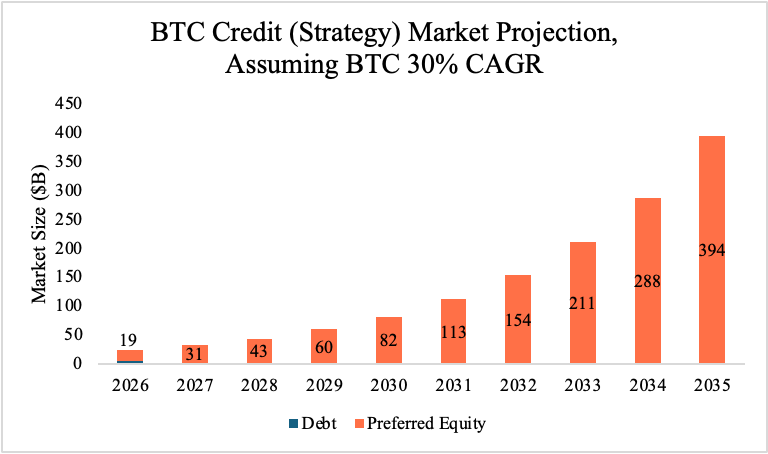

Looking ahead, the BTC credit market is projected to reach $394 billion by 2035, growing at an estimated 40% compound annual rate, assuming Bitcoin maintains a 30% CAGR and MicroStrategy continues to peg roughly 25% of Bitcoin credit issuance to NAV.

As the Bitcoin credit market balloons, USDat stands at the epicenter of a new financial frontier, transforming Bitcoin’s dormant collateral into a global engine for stable yield. By holding sUSDat, users exchange some of Bitcoin’s upside for consistent, yield bearing returns supported by institutional grade credit, effectively insulating themselves from the volatility of market cycles.

In other words, USDat yield is scalable because it stems from Bitcoin’s structural alpha: the integration of a hard digital asset into mainstream financial infrastructure. The result is a real, enduring yield born from the alignment of two financial systems.

Why the Yield Is Durable

Most high-yield products in crypto fail for the same reason: they depend on short-term momentum and fragile on-chain leverage. When markets turn, these systems collapse almost instantly.

USDat’s structure is fundamentally different. Our Bitcoin Credit strategy is at least 4x overcollateralized in Bitcoin across all credit holdings. And unlike typical DeFi borrowers, our borrowers are institutional entities ****- with access to deep, diversified capital markets - not retail traders or overleveraged on-chain vaults.

This difference is what makes USDat’s yield durable.

During bull markets, anyone can make interest payments. In bear markets, only borrowers with real access to capital markets can. In these periods, DeFi is willing to take yield haircuts in favor of consistent, safer assets. We believe that STRC - and thus sUSDat - will flip this paradigm, offering double-digit yields across market conditions.

MicroStrategy, an $80B public company, exemplifies that kind of durability. It has multiple, proven ways to manage liquidity and meet obligations, regardless of market conditions:

Issuing new equity to fund interest payments;

Refinancing through convertible notes or preferred equity to extend maturities and smooth cash flows;

Selling portions of its Bitcoin holdings into highly liquid markets.

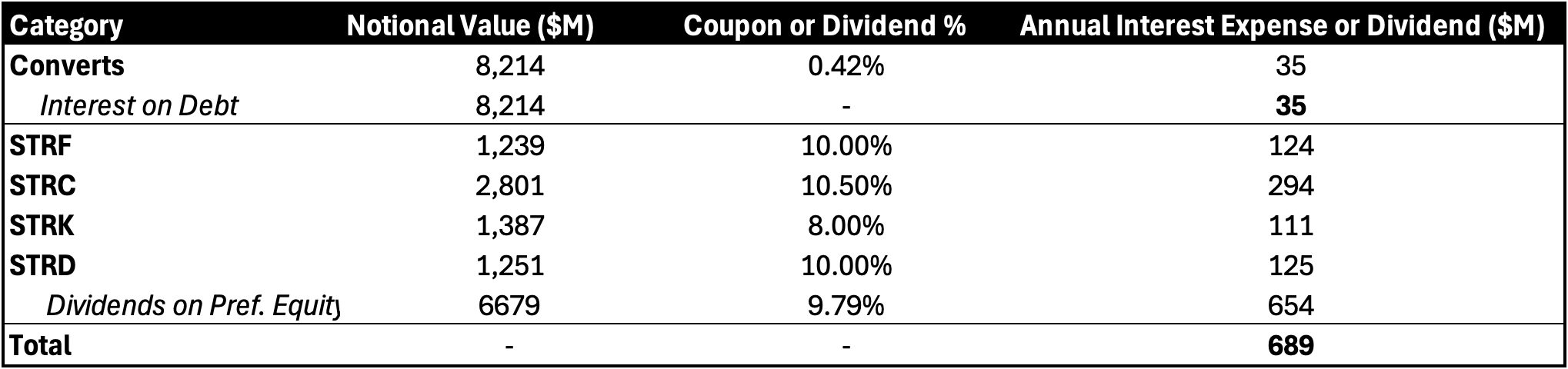

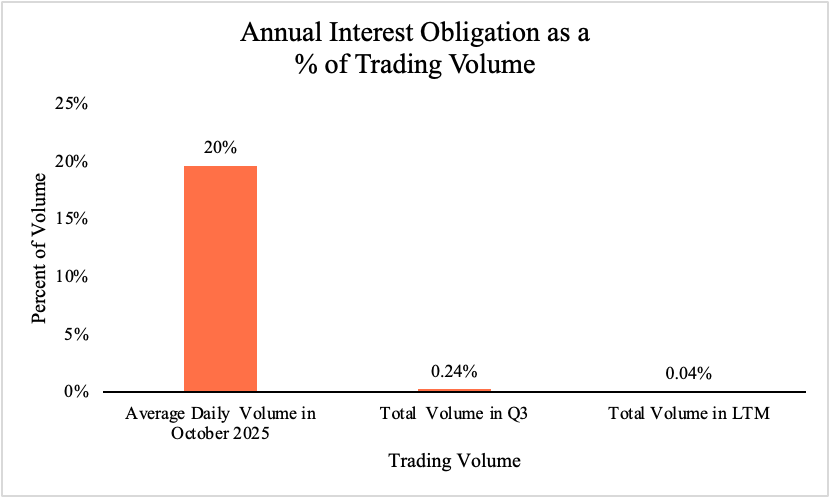

As shown in the table above, MicroStrategy’s total annual interest and dividend obligation is $689 million, an amount it can easily cover through multiple channels.

For example, issuing equity equal to $689M would represent only ~20% of its average DAILY trading volume in October 2025, a negligible dilution if spread across the year. The same payment equals 0.24% of Q3 total trading volume and just 0.04% of total trading volume LTM.

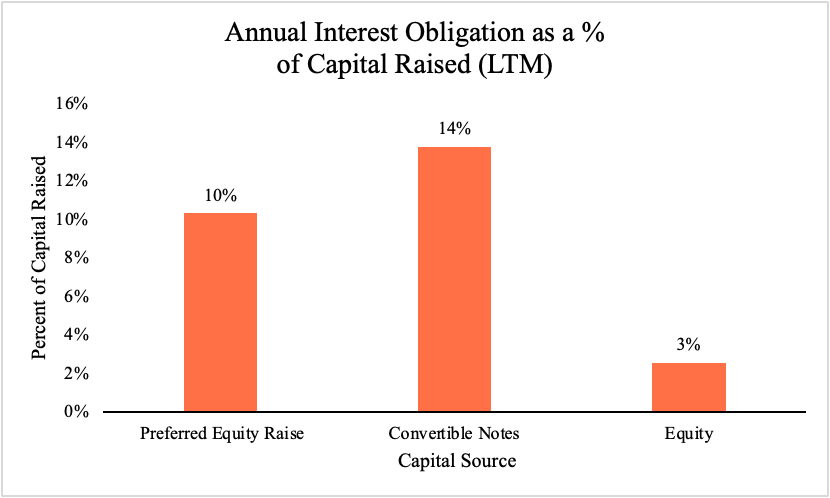

Beyond equity, MicroStrategy can uses convertible notes and new preferred equity issuance for financing. The current annual obligation amounts to just 3% of capital raised via equity over the last 12 months, 10% of preferred equity raised, and 14% of convertible notes issued, a small fraction of its demonstrated capital-raising capacity.

It is worth noting that the liquidation preference of the credit instrument purchased by USDat (STRC) ranks second in seniority compared to other credit instruments issued by Strategy. Consequently, issuing junior credit instruments not only helps fund the interest payments on STRC but also enhances STRC’s collateral ratio. Moreover, any payment defaults would first occur among the more junior credit instruments before affecting STRC.

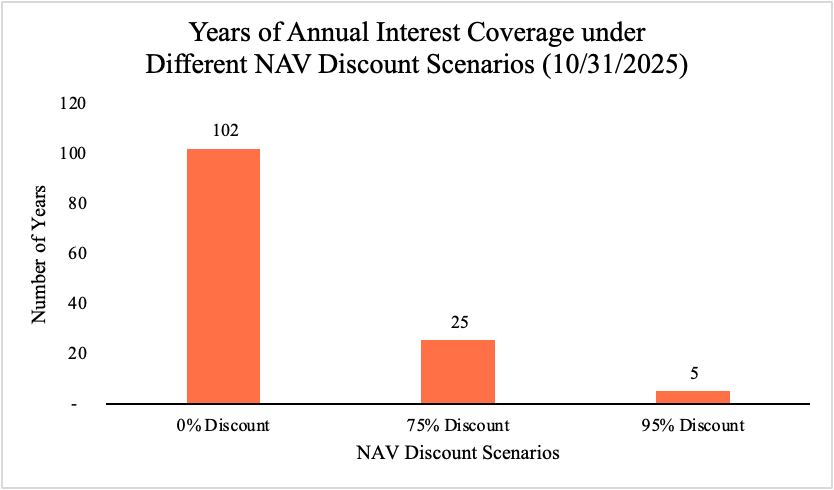

Even if MicroStrategy had to sell Bitcoin to make payments, its balance sheet remains extremely strong. With $70.6 billion in Bitcoin holdings, it could fund over 102 years of interest payments at current rates. If Bitcoin fell 75%, leaving $14.1 billion in NAV, the company could still cover more than 25 years of obligations. Even in a 95% drawdown, it could fund five full years of payments from NAV alone.

In reality, MicroStrategy would likely use a mix of these tools - equity, preferred equity, convertible debt, and appreciated Bitcoin sales - to optimize financing. The point is simple: it has options, and it can pay easily.

This financial flexibility gives USDat’s counterparties - and, by extension, USDat’s users - exceptional confidence. USDat’s yield system isn’t built on speculative leverage or market hype. It’s backed by institutional borrowers with deep, proven access to capital and financial tools to manage risk. This is a yield model designed not for short-term expansion, but for long-term endurance through any market cycle.

Managing Counterparty Risk: Strength Through Diversification

All credit carries counterparty risk, but USDat’s model is built to manage it intelligently, not to pretend it doesn’t exist. While MicroStrategy is currently our primary borrower, our long-term objective is to diversify exposure across multiple DATs.

That said, size and quality matter. Larger, well-capitalized borrowers have stronger access to liquidity and financing during periods of market stress, adding a critical layer of protection to USDat’s ecosystem. By expanding our institutional borrower base methodically, prioritizing financial strength and transparency, USDat aims to strike the right balance between diversification and credit quality, creating a foundation for sustainable, transparent yield in the convergence era.